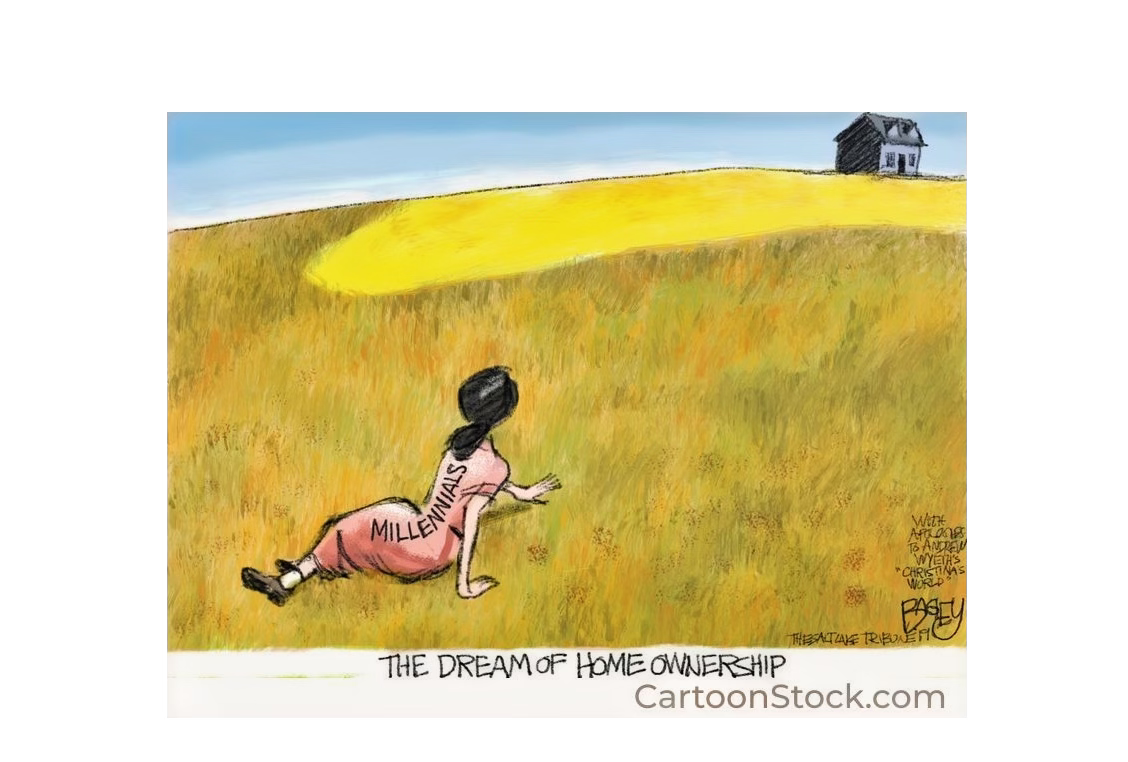

There’s a strange, almost invisible trade-off that has unfolded over the past twenty years, and most young adults never realized they were participating in it. Many people talk about the housing crisis: too little supply, high demand, zoning that borders on impossible, and prices in places like Santa Barbara that feel more like fantasy than economics. A…

Keep reading with a 7-day free trial

Subscribe to Santa Barbara Current to keep reading this post and get 7 days of free access to the full post archives.